Alaska CRE Q1 2026: Vacancy, Cap Rates, What Stalled

Introduction

Alaska’s commercial real estate market closed Q1 2026 with a sharper split than the seasonal narrative of three months ago suggested. Industrial fundamentals tightened further. Retail held up at the center, but the restaurant tenants that anchor so much of it are getting squeezed by food and labor costs, and a run of closures is the visible result. Downtown Anchorage office moved the wrong way, not sideways. And cap rates, despite two Fed cuts in late 2025, did not compress the way investor decks predicted in January. This is our Q1 2026 Alaska commercial real estate review, written as a single catch-up piece because the story changed more than the calendar did.

What Held: Industrial Vacancy Near Record Lows

The industrial sector remained the strongest performer in Alaska commercial real estate through Q1 2026. Vacancy in modern, well-located warehouse and light-industrial product under 20,000 square feet sat near historic lows across Southcentral Alaska, particularly in the Port of Alaska, Ted Stevens International, and South Anchorage logistics corridors. [VERIFY: Anchorage industrial vacancy rate Q1 2026].

Three structural forces continue to support the sector. First, developable industrial land in Anchorage remains tightly constrained, and high construction costs push replacement rents above what existing tenants pay. Second, demand from logistics, oil and gas support, and construction materials has been steady, with no Q1 softness despite the broader macro environment. Third, the Pikka project’s first oil is scheduled for Q2 2026, with roughly 1,000 workers on field gathering lines and pipelines through the past winter. That activity creates real, measurable demand for staging, fabrication, and equipment storage space across Southcentral Alaska, and it is showing up in the deal flow.

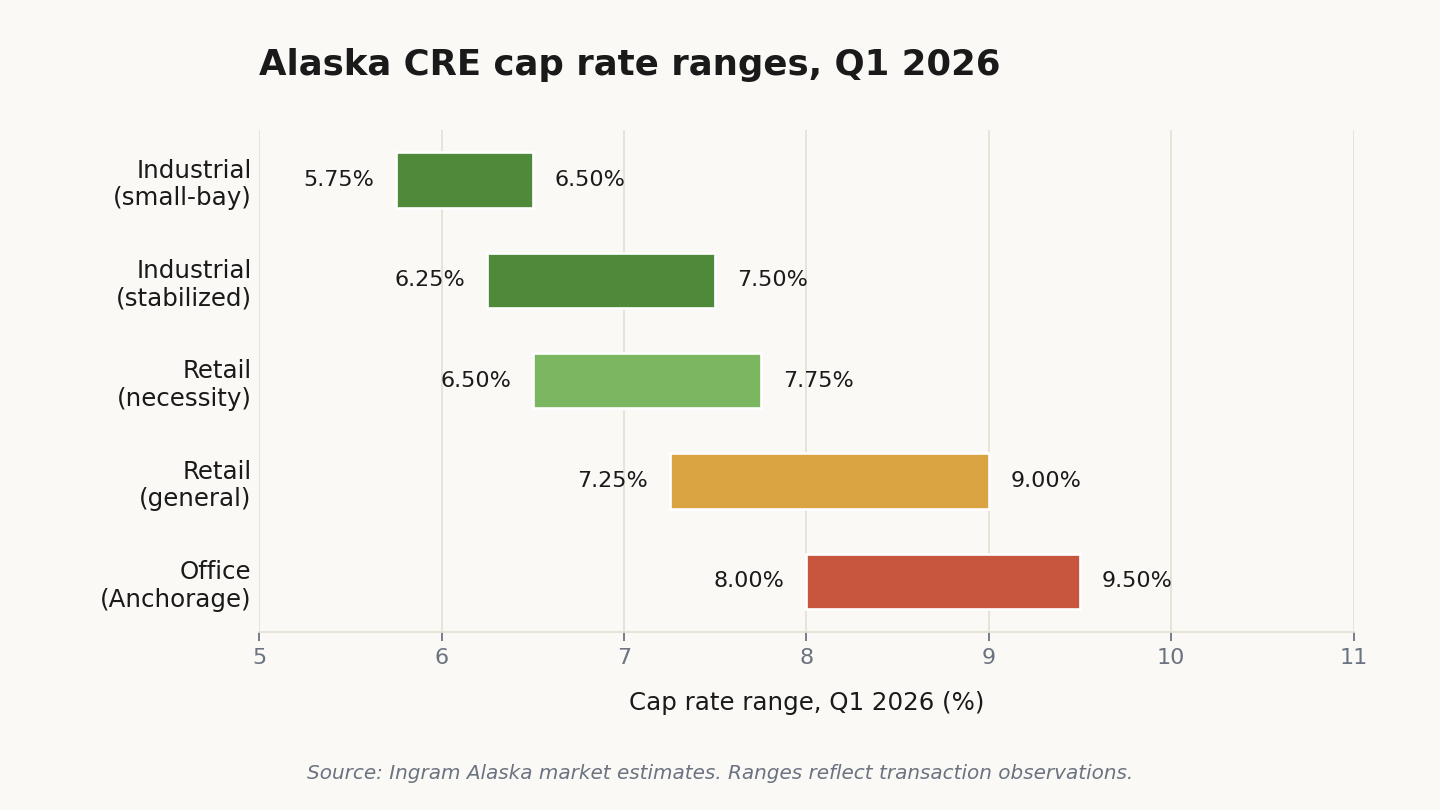

For investors, the takeaway is unchanged from the January forecast. Stabilized industrial assets in Anchorage trade at cap rates roughly in the 6.25% to 7.5% range, with small-bay product compressing tighter where leasing velocity is strongest. The structural supply story is the moat, and Q1 did not weaken it.

What Softened: Restaurant Margins and the Anchor-Tenant Problem

The softest part of the Q1 2026 picture was not a vacancy statistic. It was operating margins in food service. Restaurant operators across Anchorage are absorbing food and labor costs that have climbed faster than menu prices can follow, and for many the math no longer works. That matters to commercial real estate well beyond the operators themselves, because restaurants anchor a large share of Alaska retail. They hold down pad sites, end-caps, and multi-tenant centers, and they generate the foot traffic that neighboring tenants underwrite their own rent against. When a restaurant anchor struggles, the whole center feels it.

The visible signal in Q1 and into the spring was closures. The Dairy Queen on Abbott Road shut its doors recently, and the Wendy’s on Spenard Road closed over the winter. In late May, Williwaw Social, one of the larger bar and event venues in downtown Anchorage, closed after nearly a decade, with ownership citing rising costs and rent. Quick-service and entertainment closures do not stay contained to a single tenant. A dark drive-thru pad or a shuttered anchor pulls traffic away from the neighboring suites and weakens the next rent negotiation across the center.

Federal tariff policy and Alaska’s standing shipping premium still pressure retailers that move imported goods, and landlords should keep modeling tenant rent coverage on tariff-adjusted costs. But the near-term driver to watch is operating-cost compression on food service and the local-demand picture underneath it, not the tariff line by itself. For investors evaluating retail acquisitions, the better Q1 lens is tenant category exposure and anchor health, not headline occupancy.

Downtown Anchorage: The Submarket Under the Most Pressure

If industrial is the strongest submarket in Alaska CRE right now, downtown Anchorage is the weakest. Office vacancy downtown is elevated and has not started a real recovery, and the problem is not only the amount of empty space. It is the demand picture around it. Fewer downtown workers and fewer locals spending money downtown have thinned the customer base that street-level retail, restaurants, and service tenants depend on, which feeds back into the same anchor-tenant pressure showing up elsewhere in the market.

Public-safety perception is part of the equation. Visible homelessness and concerns about safety after business hours are weighing on tenant decisions to locate or stay downtown, and that perception is now a leasing input rather than a side conversation. The Williwaw Social closure landed squarely in this submarket. For owners of downtown office and street-level retail, the Q1 takeaway is that re-tenanting timelines are longer, concessions are deeper, and the recovery case depends on factors such as foot traffic and public safety that sit outside any single lease.

Cap Rates and the Higher-for-Longer Reality

The Federal Reserve cut rates twice in late 2025, and the federal funds range entering Q2 2026 sits at 3.75% to 4.00%. The investor expectation in January was that 2026 would deliver meaningful cap rate compression. Q1 did not deliver it.

The reason is that cap rate moves do not track the policy rate one for one. They track the 10-year Treasury, the spread investors demand for CRE risk, and the income growth assumption underwriting the deal. The 10-year has stayed elevated, the risk spread has widened modestly, and rent growth assumptions on Alaska office product are softer now than they were six months ago. Net result: cap rates on most asset classes held flat in Q1, with mild compression only on small-bay industrial and necessity-based retail.

For Alaska investors, this matters in two ways. Buyers who modeled aggressive Q1 cap rate compression to justify pricing are repricing their offers. Sellers who priced to that same compression assumption are seeing longer days on market or pulling listings. The market is not frozen, but the bid-ask spread is wider than it was in Q4 2025, and the deals closing are the ones where both sides updated their assumptions.

Mat-Su Absorption: From Speculative to Real

The Mat-Su Valley story moved from forecast to evidence in Q1 2026. Wasilla and Palmer commercial absorption is no longer a thesis about future population growth. It is a present-tense story about daytime economic activity shifting north from Anchorage. Quick-service restaurants, coffee, dental, med-spa, fitness, and convenience tenants are clustering on visibility corridors where new rooftops and improved access overlap. Small-shop space attached to a strong anchor or a drive-thru pad is leasing quickly.

The Pikka and Willow project economics overlay on top of this. Pikka first oil is targeted for Q2 2026, and Willow construction continues toward 2029 first oil. The slope workforce, contractor base, and equipment supply chain that supports these projects does not live on the slope. It lives in Wasilla, Palmer, and Anchorage. That is the demand source feeding light industrial and flex absorption in the Valley, and the Q1 leasing data reflects it. [VERIFY: Mat-Su commercial absorption Q1 2026].

One Q1 development that owners should track carefully is the Matanuska-Susitna Borough’s commercial property reassessment cycle. Several owners reported assessed value increases in the 30% to 50% range on individual commercial parcels, the result of the Borough working to correct decades of undervaluation. For owners holding NNN-leased product, the higher assessed values flow to tenants through tax pass-throughs. For owner-users and gross-lease landlords, the increases hit NOI directly. Either way, the assessment notice is now a Q2 underwriting input, not a footnote.

For more on what is driving Mat-Su’s commercial expansion, see our analysis of the Mat-Su Valley CRE boom in Wasilla and Palmer.

The Quiet Compressor: Insurance and NNN Pass-Through Friction

The least-discussed Q1 2026 story is also the one most likely to shape leasing conversations through the rest of the year. Alaska commercial property insurance premiums continued to escalate, driven by earthquake risk, rebuilding cost inflation, and a tightening reinsurance market. Insurance is now a meaningful enough operating expense line that it changes how landlords structure leases and how tenants evaluate them.

The market response has been a continued shift toward triple-net (NNN) lease structures, particularly on retail and industrial product where landlords need to recover rising operating expenses without disrupting headline rent. The friction shows up at lease execution, when tenants compare a NNN proposal in Anchorage against a gross or modified-gross structure in a Lower 48 market and find the all-in cost is closer than the base rent suggests.

For tenants, the Q1 lesson is that the comparison that matters is total occupancy cost per square foot, including insurance, snow removal, heating fuel, and tax pass-throughs. For landlords, the lesson is that the NNN structure only protects margin if the lease properly defines what is and is not passed through. Loose definitions on insurance pass-throughs in particular are creating tenant disputes mid-term.

What This Means for Investors, Owners, and Tenants

The Q1 2026 picture is not a single market. It is four markets moving at different speeds.

Industrial investors should keep buying or holding well-located small-bay product in Southcentral Alaska. The structural supply constraint is intact, the slope-driven demand is real, and the cap rate floor is supported by genuine fundamentals rather than rate optimism.

Retail and food-service landlords should re-underwrite anchor-tenant health first, stress-testing restaurant operators on food and labor cost compression, then layer tariff-adjusted assumptions for imported-goods tenants. The right opportunities are still there, but the wrong ones will not show up as obvious in the rent roll.

Office investors should underwrite downtown Anchorage conservatively. Vacancy is elevated, the demand and public-safety picture is working against a quick recovery, and pricing should reflect a longer hold and deeper concessions than the January forecast assumed. Better-located suburban and medical office continues to hold up far better than the downtown core.

Mat-Su investors should treat the absorption story as evidence-based, not speculative. Underwrite to current rent growth, not projected, and price the property tax reassessment cycle into the operating model.

Tenants in any sector should engage early on lease renewals, scrutinize NNN pass-throughs at execution, and pressure-test the all-in cost of occupancy across multiple location options. The market is no longer giving away leverage on either side.

For investors evaluating specific opportunities or owners considering a sale, our investment sales practice walks through deal-level cap rate, NOI, and underwriting analysis grounded in current Q2 2026 market conditions.

Contact Ingram Alaska

Looking for Alaska commercial real estate market intelligence, investment opportunities, or tenant representation in 2026? Ingram Alaska has facilitated high-profile commercial real estate transactions across Anchorage, the Mat-Su Valley, and the rest of the state for over 20 years. Whether you are evaluating an industrial acquisition, repositioning a retail asset, or negotiating a lease in a tighter market, we bring the data and the deal-flow relationships to get it done.

Phone: (907) 830-7319 Email: info@ingramalaska.com